How Our Family Earns Millions of Points Faster — The Business Credit Card Secret Most Parents Miss

When I tell people that our family of 4 flies business class to places like Peru without paying cash, the first question is always: "How do you earn THAT many points?"

The honest answer? Business credit cards.

Not because I run some massive corporation. Because I've been selling clothes, kids' stuff, and upcycled furniture on eBay, Poshmark, and Facebook Marketplace for over 10 years. That side hustle, one that millions of parents are already doing, qualifies me for some of the most powerful points-earning cards available.

And most families have no idea this strategy exists.

Here's everything you need to know about business credit cards, why they're the secret weapon for family travel hackers, and how to figure out if you already qualify right now.

🎥 Watch: How to Get a Business Credit Card as a Side Hustler (Full Walkthrough)

Prefer to read? Keep scrolling for the full written guide with all the details.

DO YOU ACTUALLY QUALIFY? (SPOILER: YOU PROBABLY DO)

This is where most parents stop reading because they assume business credit cards aren't for them. But here's the truth: if you've ever made money outside of a regular W-2 job, even a little, you likely already qualify.

Banks define "business" much more broadly than most people think. You don't need an LLC, employees, a registered business name, or even consistent income. You need to be doing something with the intent to earn money.

That includes:

Selling on eBay, Poshmark, Facebook Marketplace, Mercari, or Etsy

Driving for DoorDash, Uber Eats, or Instacart

Babysitting, tutoring, or dog walking

Freelance writing, photography, or consulting

Running a blog or YouTube channel with the goal to monetize

Renting out a room on Airbnb or a car on Turo

I've personally been selling secondhand clothes, my kids' outgrown items, and upcycled furniture on resale platforms for over 10 years. That's my business. It's legitimate, it's real, and it's what I use when I apply for business credit cards.

If any of the above describes you, keep reading, because this strategy is about to change how fast your family earns points.

WHY FAMILIES NEED BUSINESS CARDS MORE THAN ANYONE

Here's something the big points and miles websites don't talk about enough: earning enough points for solo travel is relatively easy. Earning enough points to fly a FAMILY OF 4 in business class? That's a completely different challenge.

Think about it. A solo traveler needs 60,000 points for a business class flight to Europe. A family of 4 needs 240,000 points for the same trip. That's four times the earning power required.

Business credit cards are how families close that gap. Here's why they're so powerful:

Massive welcome bonuses.

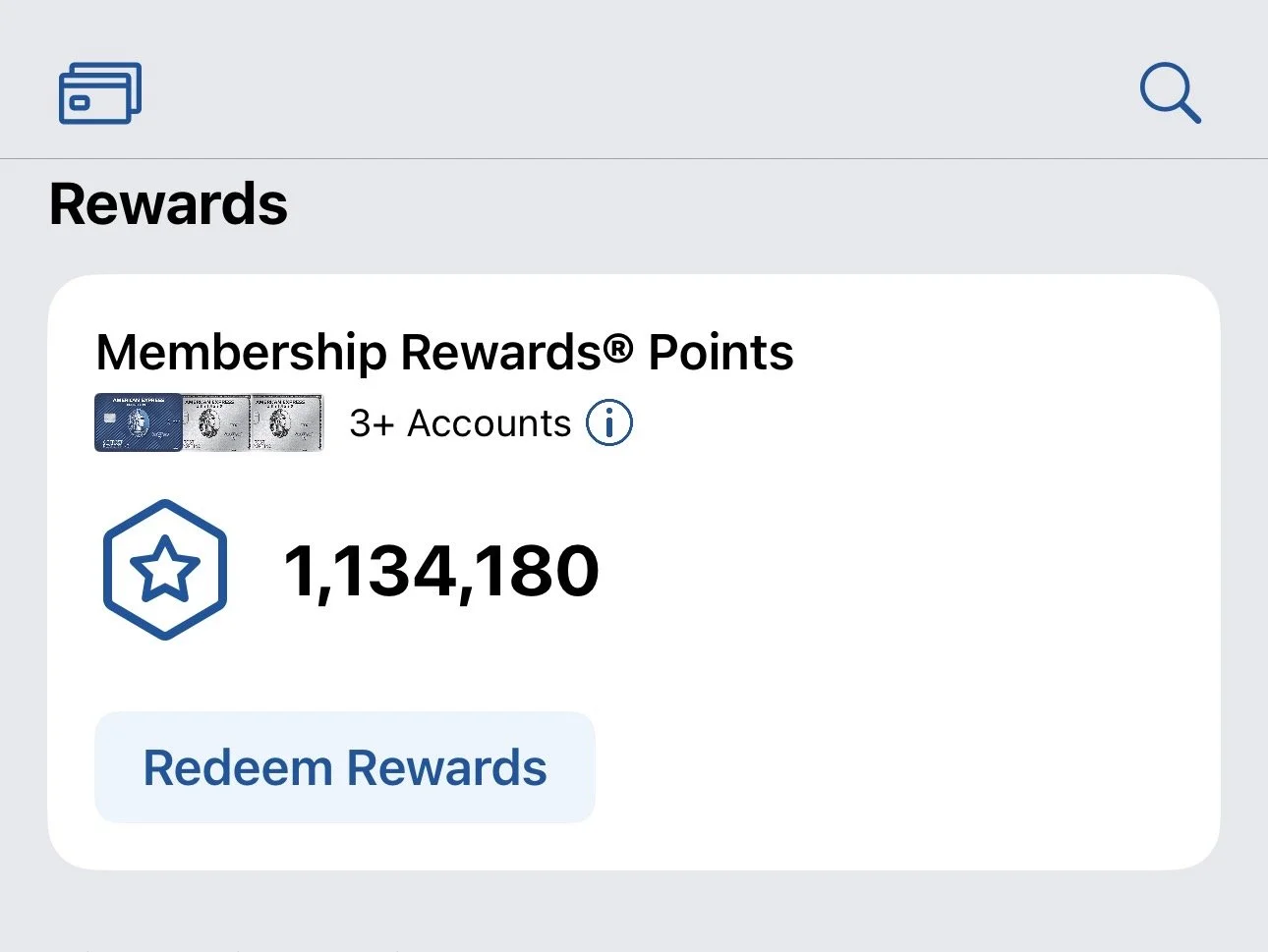

Business cards routinely offer 75,000 to 120,000+ point bonuses after meeting a minimum spend. As a family you're already spending on groceries, gas, kids' activities, and household needs. Meeting a $6,000 minimum spend in 3 months is much more realistic for a family than for a single person. I've earned well over a million points just from welcome bonuses on business cards alone.

My current Amex membership rewards balance earned mostly from business credit cards

They don't count against Chase 5/24.

This is the single biggest reason every family travel hacker needs business cards. Chase's 5/24 rule means they'll deny you if you've opened 5 or more personal cards in the last 24 months. But most business cards don't show up on your personal credit report — which means they don't count toward your 5/24 limit. You can hold 8 business cards and your 5/24 count might still be zero. For families trying to maximize welcome bonuses this is a game changer.

Bonus categories personal cards miss.

Many business cards earn 5x points at office supply stores, which means you can buy gift cards there and effectively earn 5x on everyday purchases. Others earn 4x on the top two categories you spend most in each month. As a family with high spending in multiple categories, these multipliers add up fast.

They keep your points ecosystem healthy.

The best points strategy isn't one great card… It's a stack of complementary cards working together. Business cards let you build a powerful earning setup without maxing out your personal card applications.

THE BUSINESS CARDS I PERSONALLY USE AND WHY

I'm not going to recommend cards I don't actually hold. Here's what's in my business card stack and why each one earns its place:

Chase Ink Business Cash

This is my office supply store workhorse. 5x points on office supply stores means I can buy gift cards strategically and earn 5x on purchases I'd be making anyway. No annual fee makes this a permanent keeper.

Chase Ink Business Unlimited

My is a good catch-all card when I want to stock up on Chase Ultimate rewards points for anything that doesn't have a better bonus category elsewhere. 1.5x on everything with no annual fee. The welcome bonus alone, typically 75,000-90,000 points, is worth the application.

Chase Ink Business Preferred

The premium Chase business card. 3x on travel, shipping, advertising, and more. The welcome bonus is often 90,000 points which at minimum is worth $900 in travel, but can be worth significantly more when transferred to airline partners.

Read More: Chase Ink Business Preferred Review

American Express Business Gold

This card earns 4x points in your top two spending categories each billing cycle automatically. For a family with high dining and gas spending this is exceptional. The annual fee is worth it when you're maximizing those 4x categories.

Read More: American Express Business Gold Review

American Express Business Platinum

My premium Amex business card. The annual fee is significant but the credits, lounge access, and point multipliers more than justify it when you know how to use the benefits.

Read More: American Express Business Platinum Review

American Express Blue Business Plus

This is my true catch-all card. 2x Membership Rewards points on absolutely everything up to $50,000 in spend per year with no annual fee. When I have a purchase that doesn't fit a bonus category on any other card, this is what I reach for. Amex Membership Rewards points are incredibly flexible with a long list of airline and hotel transfer partners, so every point earned here has serious value.

Citi AAdvantage Business World Elite

For American Airlines redemptions specifically. Having airline-specific business cards gives me flexibility when transferable points don't have good availability.

Wyndham Earner Business

An underrated card that earns Wyndham points at an exceptional rate. For families who stay at Wyndham properties or want to transfer to Caesar's Rewards for Las Vegas stays this card earns its keep.

The key takeaway: I didn't get all of these at once. I built this stack strategically over time, spacing out applications and always making sure each card earns back its annual fee before keeping it.

HOW TO APPLY AS A SOLE PROPRIETOR STEP BY STEP

Applying is simpler than you think. Here's exactly how to fill out a business card application when your business is a resale side hustle or similar:

Business name: Use your legal name. If you sell on Poshmark under your own name, that IS your business name. No LLC required.

Business structure: Select Sole Proprietorship.

Federal Tax ID: Use your Social Security Number. You don't need an EIN unless you have employees.

Business start date: When did you start your side hustle? For me that's over 10 years ago. Even if you just started selling on Facebook Marketplace last year, that's your start date.

Annual revenue: What did you actually earn last year? Be honest. Even $500 in Poshmark sales counts. If you're just starting, a reasonable projection is fine.

Business address and phone: Your home address and personal phone number are perfectly acceptable.

Number of employees: Zero if it's just you.

Business category: Pick the closest match. For resale sellers try Retail → Miscellaneous Retail → Used Merchandise. For content creators try Media or Advertising.

One important note: be completely honest on your application. You're not gaming the system. You're accurately describing a real business activity that qualifies under the bank's own definition. That's it.

WILL YOU GET APPROVED?

Approval for sole proprietor business cards comes down almost entirely to your personal credit score and history, not your business revenue. Banks understand that small and new businesses are common.

You generally have a solid shot at approval if you have:

A personal FICO score of 680 or higher

A clean payment history with no recent late payments

Reasonable personal credit utilization

You do NOT need:

A registered business name or LLC

Business tax returns

An EIN

A website

Significant business revenue

The biggest mistake I see families make is assuming they won't qualify because their side hustle feels too small. Banks approve new and tiny businesses all the time. Don't let imposter syndrome stop you from earning the points that fund your family's adventures.

IMPORTANT THINGS TO KNOW BEFORE YOU APPLY

Not all business cards are created equal for 5/24 purposes.

Most major bank business cards don't report to your personal credit, but there are exceptions. Business cards from TD Bank, Discover, and some Capital One business cards DO report to your personal credit and will count against your 5/24. Always verify before applying.

Space out your applications.

Don't apply for 5 business cards in a month. Build your stack gradually, giving each card time to report before your next application.

Always pay in full.

The interest on carrying a balance will erase every reward you earn. Business credit cards are only a strategy if you pay them off completely every month.

Meet minimum spends organically.

As a family you likely have enough natural spending to meet most minimum spend requirements. Don't manufacture spending beyond what you'd naturally spend.

THE BEST STARTER BUSINESS CARDS FOR FAMILY TRAVEL HACKERS

If you're new to business cards I'd suggest starting with one of these three because they have no annual fee, strong welcome bonuses, and fit naturally into a family's spending:

Chase Ink Business Cash — Best for families who shop at office supply stores or want 5x on specific categories.

Chase Ink Business Unlimited — Best for families who want a simple flat-rate earning card with a massive welcome bonus.

American Express Blue Business Plus — Best for families who want 2x Membership Rewards points on everything with no annual fee.

Once you're comfortable with business cards and understand how they fit into your overall points strategy, consider leveling up to the Chase Ink Business Preferred or American Express Business Gold for even more earning power.

BOTTOM LINE

If your family is serious about traveling on points, business credit cards aren't optional, they're essential. They're how families earn enough points to actually move the needle on free travel for 4 people instead of 1.

And if you've been selling anything on eBay, Poshmark, Facebook Marketplace, or Etsy… Or driving for a gig app, freelancing, babysitting, or running any side hustle at all… you already have a business. You already qualify.

The only question is how many more points your family could be earning.

Ready to build your business card stack?

Start with my free Beginner's Guide to Points and Miles to understand how all the pieces fit together before you apply.