Mesa Card Shutdown: What Happened, the Warning Signs We Missed, and the Lessons for Points & Miles Users

Yesterday, on Dec 12, 2025, Mesa cardholders experienced one of the most abrupt and complete shutdowns we’ve seen in the points and miles space.

Every single Mesa cardholder was affected.

Mesa shut down all cards at once, removed transfer partners, and left cardholders scrambling to protect whatever value they could, with no guidance from Mesa itself.

I was personally affected by this shutdown, and in this post I want to document what happened, what we know, and the broader lessons this situation highlights for anyone earning points with newer fintech credit cards.

The Shutdown: What Actually Happened

Mesa executed a full, across-the-board shutdown of its credit card program.

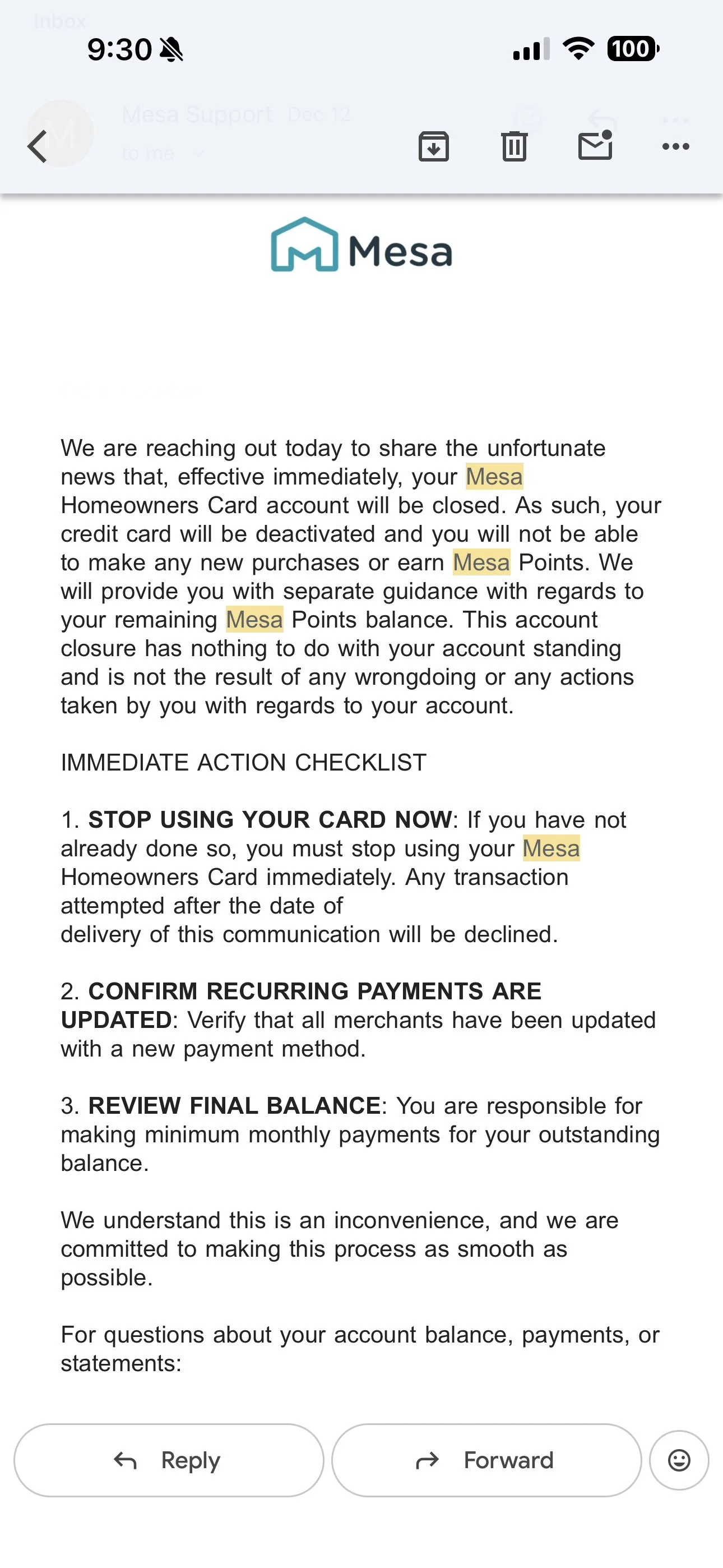

All cardholders received an email stating that:

Their Mesa card account was being closed

The closure was “through no fault of your own”

Access to key features — including transfer partners — was removed

There was:

No warning

No transition period

No phased wind-down

Cards that had worked recently — sometimes even earlier that same day — suddenly stopped working.

This was a total program shutdown, not an account-by-account action.

Confusing Declines Around the Time of the Shutdown

About a week before this shutdown, some cardholders noticed inconsistent declines, even before receiving the closure email. This happened to me when trying to make a property tax payment. Other people experienced large transactions failing, meanwhile, smaller everyday purchases (like groceries) sometimes still worked

These declines were not consistent or predictable, and at the time many cardholders assumed they were:

Temporary glitches

Merchant coding issues

Or problems related to Mesa being a small fintech team

In hindsight, these may have been early operational warning signs, but there was no indication that a complete shutdown of all accounts was imminent.

What Happened to Points After the Shutdown

Once every account was closed, cardholders were left with confusing redemption outcomes:

The ability to transfer points to travel partners was suddenly gone

Some people were able to cash out points as a statement credit at approximately 0.6 cents per point

Others saw no redemption options at all

Later, posts surfaced in private groups and then mainstream Facebook groups describing an unofficial workaround that temporarily allowed some users to access transfer partners again

The workaround was not official and it did not work for everyone. Some users never saw the option.

Others were unable to cash out or transfer and were simply stuck

Because all cardholders were shut down simultaneously, there was widespread concern that unredeemed points could disappear entirely.

I personally redeemed 102,000 points for approximately $618.

This REALLY hurt, but I chose to do this in order to minimize my losses in case I lost all of my points. Then a few hours later, people were discussing the work around for getting the transfer partner page to show up on the app. In hindsight, I wish I would have waited and then tried to transfer my points to Air Canada Aeroplan, but in situations like this, you can never predict what the best thing to do is, and I would rather end up with real cash in my pocket vs $0 at the end of the day.

What the Mesa Card Offered (Before the Shutdown)

Before this happened, Mesa stood out as an unusually generous card, especially given that it had no annual fee.

Key features included:

No annual fee

Multiple statement credits

3x points on several high-value categories

The ability to transfer points to travel partners

For a no-fee card, this value proposition was extremely aggressive.

The Earning Structure That Felt Almost Too Good

Mesa offered 3x points in categories that are expensive for issuers to support long-term like daycare, home improvement, utilities, taxes, etc.

Over time, some cardholders also noticed that purchases outside the advertised categories earned 3x as well.

In my case, I noticed that a liquor store in my area was earning 3x points on purchases

At the time, many users, myself included, assumed this was due to Mesa being run by a small team, growing pains with this new product being on the market, or imperfect merchant coding.

Signup Bonuses, Referrals, and the Frozen Waitlist

Mesa’s customer acquisition strategy also raised questions.

Mesa briefly offered a 50,000-point signup bonus earlier in 2025 (around May/June) with a $5,000-in-3-months spend requirement. Cardholders reported that the window was very short, advertised through the end of June but pulled early, making it easy to miss if you weren’t watching closely or didn’t sign up immediately.

After the original welcome offer was pulled, Mesa shifted to a referral-based pathway to earn a similar bonus. Under this structure, cardholders could earn 5,000 points per approved referral, and once two referrals were successfully completed, a separate spend-based bonus would unlock inside the app. That unlocked offer allowed the cardholder to earn 50,000 additional points after spending $10,000 within 90 days, provided the offer was manually activated. On paper, this created a way to earn a large bonus without reopening public applications.

What ultimately made this referral-based bonus difficult, and for many people impossible, to achieve was not the spending requirement, but the fact that Mesa stopped accepting new applications. Shortly after this referral structure was introduced, Mesa paused new signups and placed prospective applicants on a waitlist. That waitlist remained frozen for months, meaning existing cardholders were encouraged to refer others but had no practical way to complete those referrals. As a result, the referral-locked bonus technically existed, but for many users, the path to earning it was effectively blocked.

Why This Was So Risky for Cardholders

Although Mesa was backed by Celtic Bank, it’s important to understand:

Points are not bank deposits.

They are:

Unsecured liabilities

Governed by program terms

At risk if a program shuts you down or goes out of business suddently

Because Mesa closed every account at once, unredeemed points were immediately at risk.

What This Taught Me About Speculative Transfers

In general, I do not recommend speculative transfers.

Once points leave a bank program:

They can’t be reversed

They’re subject to airline or hotel program rules

They may expire or devalue

However, this situation highlights an important exception:

If a bank or fintech program shuts down or closes your account, you can lose your points entirely.

How Major Banks Typically Handle Closures

Chase usually provides a grace period to transfer points

Amex technically allows 24 hours, but many people struggle:

Transfer partners must already be linked

Transfers can fail or take too long to process

Customer support agents are not always able to help you transfer out your points and some people are stuck losing their points entirely or cashing out for giftcards at poor value.

In hindsight, while I don’t generally recommend speculative transfers, I wish I had transferred my Mesa points to Air Canada Aeroplan when transfers were still available, because this is a program I know I would have used.

The Core Lesson: Points Have No Value Until You Use Them

This shutdown reinforces one of the most important truths in points and miles:

Points don’t have real value until they’re redeemed.

Unredeemed points always carry risk, especially in newer or less established programs.

Key takeaways:

Fintech programs can shut down overnight

“Too good to be true” value often comes with tradeoffs

Hoarding points increases exposure to total loss

Sometimes protecting value matters more than chasing maximum upside

What Mesa Said About Remaining Points

In the shutdown email, Mesa stated that they would be providing separate guidance regarding remaining points. As of now, it’s unclear what that guidance will look like or whether additional redemption options will be offered.

Because of that uncertainty, many cardholders chose to cash out their points immediately as a statement credit rather than risk losing them entirely. I did the same.

That said, if Mesa ultimately allows point transfers to travel partners again, I plan to ask whether previously redeemed statement credits can be reversed so those points can be transferred instead. It’s far from guaranteed, but when it comes to points, it never hurts to ask in an effort to preserve as much value as possible.

Final Thoughts

The Mesa shutdown wasn’t the result of misuse, gaming, or cardholder behavior. Every account was closed at once without any notice. That distinction matters, especially for people new to points and miles who may worry that situations like this are caused by doing something “wrong.”

More importantly, this wasn’t just a Mesa story; it’s a reminder of the unique risks that come with newer fintech rewards programs.

These cards often launch with aggressive value propositions, generous earning rates, and eye-catching bonuses to attract early adopters. But unlike established bank programs, they can also change direction (or disappear) far more quickly.

That doesn’t mean fintech cards should be avoided entirely. It does mean they should be approached differently. Points earned through newer or less-established programs carry more uncertainty, and hoarding large balances in those ecosystems increases exposure to sudden loss. In contrast, established programs tend to offer clearer protections, communication and, at minimum, some form of wind-down period.

The biggest takeaway from this experience is simple: points only have value once you use them. Until then, they’re just a “promise”; one that can be altered, restricted, or removed altogether. Protecting value doesn’t always mean maximizing it. Sometimes it means making a conservative choice with incomplete information.

Mesa may still provide additional guidance, and if further redemption options become available, I’ll pursue them. But regardless of how this specific situation ends, the lesson remains the same: understand the risks, stay flexible, and don’t let the pursuit of “perfect” redemptions prevent you from protecting real value when circumstances change.

In points and miles, the best redemption is the one you actually get — before you get shut down.

New to Points & Miles?

If you’re just getting started and want a clear, beginner-friendly framework for earning and using points responsibly, grab my free guide here:

👉 MilesWithMary.com/beginners-guide