Amex Platinum vs Venture X vs Chase Sapphire Preferred: Justifying Annual Fees & Earning Rewards

Okay, so you see a credit card with an annual fee that could cover a weekend getaway, and your gut reaction is probably, "Nope!" Paying just for the privilege of swiping? It feels a bit like paying for air, right? Especially when there are so many no-fee cards out there. So, why would anyone in their right mind fork over serious cash for one of these "premium" cards?

That initial "hard pass" feeling? Totally get it. But hear me out. Those annual fees on the top-tier travel cards? They're not just random numbers they pulled out of a hat. Think of them as a VIP pass – a golden ticket that unlocks a surprisingly awesome set of perks, reward systems, and experiences designed to give you back way more value than you initially spent. At least, that's the deal for those of us whose spending habits and travel dreams line up with what the card offers. Instead of seeing that fee as money gone forever, picture it as investing in a travel-hacking superpower. For the savvy spender, these fees can be totally outsmarted, and you can even end up making money – making your credit card actually profitable.

We're going to break down why these fancy cards are more than just shiny. We'll show you how these heavy hitters, specifically the Chase Sapphire Preferred Card, the Capital One Venture X Rewards Credit Card, and The Platinum Card from American Express, can totally justify their annual price tags and deliver some serious value. Our journey involves looking at the cold, hard cash-back credits that chip away at the fee, the rewards that turn your everyday spending into free trips, the travel perks that make you feel like a travel pro, the crucial skill of using your points like a boss, and finally, a simple way to figure out if this whole thing actually makes sense for you. These three cards, each with its own vibe and price point, are perfect examples of how to flip a perceived cost into a seriously smart financial move.

Getting Your Money Back: The Magic of Statement Credits

The easiest way to chip away at that annual fee is through the statement credits a lot of these premium cards have. These credits are basically rebates for stuff you probably already buy, directly lowering how much the card really costs you. Their value is usually pretty obvious, making them a great first step in figuring out if a card is worth it. However, sometimes these cards offer credits for places that you would not normally shop at, so you can’t always calculate these credits at face value.

Some cards keep it easy with credits that take a big chunk out of the annual fee without making you do a ton of extra work.

Capital One Venture X Rewards Credit Card ($395 Fee): This card gives you up to a $300 Annual Travel Credit for bookings through their Capital One Travel portal. If you're already spending at least $300 a year on flights, hotels, or rental cars through their site, then your $395 fee just dropped to a much nicer $95. Additionally, you receive a 10,000-mile anniversary bonus every year that you keep the card. Since those Capital One miles are worth at least a penny each for travel, that's another $100 (minimum!) in value. Put that $300 credit and the $100+ bonus together, and suddenly that $395 fee looks like it owes you money before you even think about the actual rewards you earn or any other cool perks.

Chase Sapphire Preferred Card ($95 Fee): Sitting at a more wallet-friendly fee level, the Sapphire Preferred offers a $50 Annual Hotel Credit. Just like the Venture X, you need to book through their Chase Ultimate Rewards travel portal. While $50 isn't going to fund your next vacation on its own, it does cut your $95 fee by more than half, down to just $45 if you book even one hotel stay costing $50 or more through their site each year. It's a pretty easy way to get a good chunk of the fee back without changing your online booking habits much. You also currently receive $10 in Doordash credits each month and free Dashpass membership, reportedly until 2027.

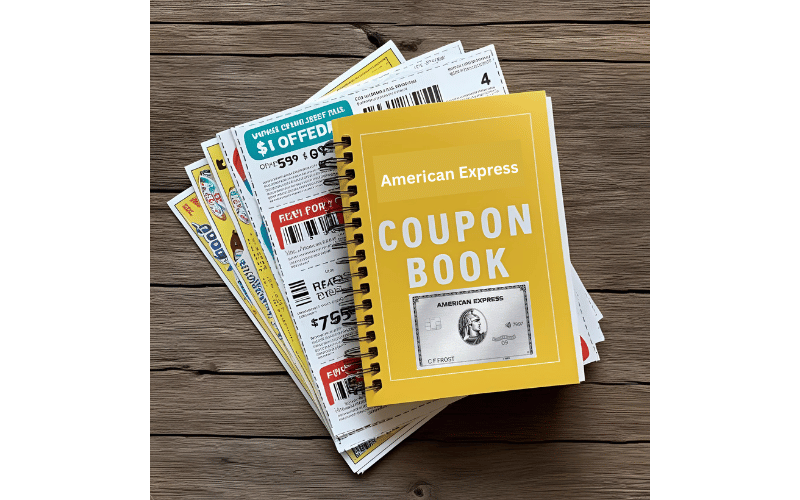

Amex Platinum's "Coupon Book" ($895 Fee)

The Platinum Card from American Express takes a different approach, often jokingly called a “coupon book” because of its long list of very specific statement credits. With the refreshed version of the card, the annual fee is now $895, and the potential value of the credits is bigger than ever. But actually getting that value still depends on whether your spending naturally matches the exact merchants and timelines Amex is targeting. In other words: this card can be amazing… or it can feel like a high-maintenance spreadsheet hobby.

Let’s look at some of these “coupons”:

$600 Hotel Credit (2 x $300):

Get up to $300 back twice per year (Jan–Jun and Jul–Dec) on prepaid Fine Hotels + Resorts (FHR) or The Hotel Collection (THC requires a 2-night minimum) booked through Amex Travel.

$200 Airline Fee Credit:

You pick one airline a year, and technically it only covers those annoying extra fees like checked bags or seat assignments – not the actual plane ticket. You need to be strategic about your airline and those little charges. (There are ways to game this credit and make it more valuable).

Up to $300 Digital Entertainment Credit:

Up to $25 per month back for select streaming services like Disney+, Hulu, The New York Times, etc. Great if you already subscribe and have these bills.

$155 Walmart+ Credit:

Covers a Walmart+ membership. This is a great perk itself because in addition to the discounts on gas and free delivery, Walmart+ members get a free subscription to Paramount+ or Peacock Premium.

$200 Uber Cash:

$15 per month plus a $20 bonus in December for Uber rides or Uber Eats in the U.S.

$100 Saks Credit:

Two $50 credits per year for Saks Fifth Avenue or saks.com.

Up to $300 Equinox Credit:

High value, but only useful if you actually use Equinox or Equinox+.

CLEAR Plus Credit (up to $209):

Covers the annual CLEAR membership.

Global Entry or TSA PreCheck Credit:

Reimburses the application fee every four years.

“Lifestyle” Coupons

$400 Resy Dining Credit:

Up to $100 per quarter at participating restaurants on the Resy platform.

$300 lululemon Credit:

Up to $75 per quarter at lululemon.

$200 Oura Credit:

Up to $200 per year toward an Oura Ring purchase.

$120 Uber One Credit:

Up to $10 per month toward an Uber One membership.

Supercharging Your Rewards: Turning Your Spending into Free Flights (and More!)

Beyond getting some cash back on your fee, the real magic of premium travel cards is how they let you rack up points or miles super fast. High multipliers on spending, especially in those categories you hit all the time (like travel and food), mean you can earn rewards way quicker than with a basic card. It's like turning your everyday spending and vacation budgets into future free (or seriously discounted) adventures.

Chase Sapphire Preferred ($95 fee):

5X points on travel booked through Chase Ultimate Rewards (their in-house travel site).

3X points on dining (including takeout and delivery).

3X points on online grocery shopping.

3X points on select streaming services.

2X points on all other travel purchases (booked directly with airlines, hotels, etc.).

1X point on everything else.

Plus, they give you a 10% Anniversary Points Bonus based on how much you spent the previous year. Spend $25,000? Boom! Extra 2,500 points. Those solid 3X multipliers in popular categories like food and online groceries make this card a workhorse for daily life, not just for when you're jet-setting. While the 5X encourages you to use their portal, the decent 2X on other travel still rewards you for booking directly.

Capital One Venture X ($395 fee):

10X miles on hotels and rental cars booked via Capital One Travel.

5X miles on flights booked via Capital One Travel.

2X miles on everything else, everywhere, with no limits. Seriously, everything.

Those 10X and 5X rates are great if you're cool with using their portal. But the real star here is the unlimited 2X miles on all of your other spending. It's a super easy way to rack up miles on all those non-bonus category purchases. If you like simplicity and high potential returns without having to remember a million different bonus categories, this card could be great for you.

Read my full review on the Venture X

Amex Platinum ($895 fee):

5X points on flights booked directly with airlines or through American Express Travel (up to $500,000 a year).

5X points on prepaid hotels booked on amextravel.com.

1X point on everything else.

This card is a powerhouse if you drop serious cash on airfare and prepaid hotels through their approved channels. That 5X directly with airlines is a huge win for those who prefer to book directly. However, the 1X on almost everything else isn’t great compared to other premium cards, and even some no-annual-fee options. This card is definitely built as a travel rewards beast, not your everyday spending champion.

Oh, and let's not forget about the welcome bonuses! These big chunks of points you get for signing up and meeting a spending requirement (like 75,000 points for the Chase Sapphire Preferred, 75,000 miles for the Capital One Venture X, and 80,000 points for The Platinum Card from American Express). Even if you just use these points for their basic value (like a penny each), you're looking at $750-$800 or more in value right off the bat, often enough to completely wipe out that first year's annual fee.

Leveling Up Your Travel Game with Valuable Perks

Beyond the points and cash-back, premium travel cards show off with a bunch of perks designed to make your travel life way smoother, comfier, and maybe even a little brag-worthy. These benefits offer convenience, potential savings, and access that can seriously upgrade your trips. While some of these are harder to put a price tag on, their impact on your travel experience can be significant, further making those annual fees seem less scary.

Airport Lounge Access: Your Escape from the Airport Zoo

One of the best perks of a travel credit card is lounge access! Think of them as your chill zone away from the crowded terminal – free snacks, drinks, Wi-Fi, comfy chairs, and a generally less chaotic vibe.

Amex Platinum: This card gets you into American Express Centurion Lounges, Delta Sky Clubs (when you're actually flying Delta that day), Plaza Premium Lounges, Priority Pass Select lounges, Escape Lounges, and even some Lufthansa lounges. Just a heads-up, bringing guests can sometimes cost extra. For frequent flyers, the savings on overpriced airport food and drinks, plus the peace and quiet to actually get some work done or just relax, can easily add up to hundreds or even thousands of dollars a year.

Capital One Venture X: the Venture X used to be one of the best lounge-access deals on the market, but this changed on February 1, 2026. The primary card holder still gets access to Capital One’s own growing network of lounges, Plaza Premium lounges, and a Priority Pass Select membership. However, free guest access is mostly gone. Authorized users no longer get lounge access for free. You must pay $125 per year per user to give them their own lounge privileges. The bottom line is that the Venture X still offers strong individual lounge access for a relatively low annual fee, but it’s no longer the easy, family-friendly lounge solution it once was.

Chase Sapphire Preferred: With its more budget-friendly $95 annual fee, this card doesn't offer comprehensive airport lounge access as a standard perk. If lounging in style at the airport is a must-have for you, you'd probably need to look at the pricier options from Capital One or Amex.

Zipping Through Security and Immigration Like a Pro

Premium cards often help you skip those ridiculously long airport lines.

Amex Platinum & Capital One Venture X: Both these cards offer a statement credit (up to $100) to cover the application fee for either Global Entry or TSA PreCheck every 4-ish years. These programs are lifesavers for saving time at security (TSA PreCheck) and when you're coming back into the US (Global Entry). The Amex Platinum even throws in an annual credit for CLEAR Plus ($189 a year), which uses your fingerprints or eyes to zoom you through the ID check at security in many US airports.

Bottom Line: These credits are like getting your time back, which, let's be real, is priceless when you're trying to catch a flight. The Global Entry/TSA PreCheck credit is like saving $20-$25 a year in hassle. The CLEAR Plus credit on the Amex Platinum is next-level speed and convenience, worth $189 a year if you use it.

Hotel Elite Status:

Automatic elite status with hotel loyalty programs can unlock some sweet perks during your stays.

Amex Platinum: This card hooks you up with complimentary Hilton Honors Gold status and Marriott Bonvoy Gold Elite status just for signing up. Hilton Gold often means room upgrades, bonus points, and sometimes free breakfast or a food and beverage credit (depends on the hotel). Marriott Bonvoy Gold Elite gets you things like better room upgrades, late checkout, and bonus points. If you're a regular at Hilton or Marriott, these perks can potentially provide value in freebies and a more comfortable stay.

CSP & Venture X: These cards generally don't offer automatic elite status with major hotel chains as a standard perk.

Rental Car Perks:

Some premium cards offer elite status with major rental car companies.

Amex Platinum: You can sign up to get free Hertz President's Circle status, Avis Preferred Plus status, and National Car Rental Emerald Club Executive status.

Venture X: You get free Hertz President’s Circle status.

Chase Sapphire Preferred: The Chase Sapphire Preferred does not typically offer automatic elite status with major rental car companies as a standard card benefit.

Travel Insurance & Protections:

All three of these cards typically come with a set of protections like:

Trip Delay Reimbursement

Trip Cancellation/Interruption Insurance

Lost Luggage Reimbursement

Delayed Baggage Reimbursement

Primary Auto Rental Collision Damage Waiver (CDW) – Important Note: Coverage can vary. CSP and Venture X often offer primary coverage, meaning you don't have to go through your own car insurance first if there's damage. Amex Platinum's coverage can be secondary unless you pay extra for a premium option. Always double-check the fine print!

Purchase Protection.

Extended Warranty (giving you a little extra peace of mind on your purchases)

Just one instance where you actually need to use these benefits – like a flight delay that leaves you stranded overnight, a trip cancellation due to something unexpected, or damage to a rental car – can save you hundreds or even thousands of dollars.

The primary auto rental CDW, in particular, can let you confidently say "no thanks!" to the expensive insurance the rental companies try to sell you, potentially saving you $15-$30 per day on your rental. While you need to read the fine print for each card to understand the specific terms, coverage limits, and exclusions, these protections offer serious peace of mind and a financial safety net that can, in a single incident, justify the annual fee many times over.

Looking at how these perks are spread out, you can see a pretty clear pattern: the higher the annual fee, the more bells and whistles you tend to get.

The Amex Platinum, with the biggest fee, throws in the most comprehensive and luxurious set of benefits, especially when it comes to lounge access and elite status.

The mid-tier Venture X ($395 fee) gives you great value on lounge access but fewer of those elite status perks. The $95 cards generally skip the really expensive benefits, focusing more on how you earn rewards and those basic credits.

This creates different levels of cards for different travel needs and budgets. It's also important to remember that a lot of these perks require you to activate them, like picking an airline for the Amex fee credit, signing up for those hotel and car rental statuses, or applying for Global Entry/TSA PreCheck/CLEAR using the credits. The value is just potential until you take those steps, so staying on top of your benefits is key to getting the most bang for your buck.

Cashing In Those Points: The Art of Turning Rewards into Real Travel

Racking up a big pile of points or miles feels good, but the real test of a travel card's value is how well you can actually use those rewards. Earning points is only half the battle; turning them into tangible value is crucial for wiping out that annual fee and actually coming out ahead. Not all ways of using points are created equal, so being strategic here is super important.

Understanding the different ways that you can use your points is like understanding a value ladder:

Cash Back/Statement Credit: This is usually the lowest value you'll get for your points, often around 1 cent per point (cpp) or sometimes even less, depending on the card program. It's simple and straightforward, but using travel points for cash back usually means you're not getting the full potential out of them.

Travel Portals (Chase Ultimate Rewards, Amex Travel, Capital One Travel): Booking travel directly through the card issuer's website lets you use your points like cash to pay for flights, hotels, rental cars, and sometimes even activities. Points are often worth a fixed amount in the portal, usually around 1 cpp. However, some cards give you a bonus here; for example, the Chase Sapphire Preferred gives you a 25% boost, making your points worth 1.25 cpp when you book travel through Chase Ultimate Rewards. This is better than cash back and convenient for simple bookings, giving you a solid baseline value.

Transfer Partners (Airlines & Hotels): This is where the real magic happens and you can often get way more value for your points. Most premium travel card programs (Chase Ultimate Rewards, Amex Membership Rewards, Capital One Miles) let you transfer your points directly to the loyalty programs of various airline and hotel partners (think United MileagePlus, Air Canada Aeroplan, British Airways Avios, World of Hyatt, etc). This approach takes a little more effort (you need to understand the partner programs, award availability, and routing rules) and flexibility (being open to different airlines, dates, or connections), but the potential payoff in terms of value per point is significantly higher.

Real-World Examples

Let's see how different redemption strategies can play out with a welcome bonus:

A 75,000-point bonus (like from CSP) could be worth:

$750 as cash back (at 1 cpp).

$750 towards travel via the Chase portal, but up to 1.75 cpp with select Points Boost redemptions.

Potentially enough points transferred to an airline partner (like British Airways Avios for short flights on American Airlines, or United MileagePlus for domestic routes) to cover flights worth $1000+ or more (getting you 2+ cpp or more).

An 80,000-point bonus (like from Amex Platinum) could be worth:

$800 towards travel via the Amex portal (at 1 cpp for most travel).

Potentially enough points transferred to a partner like Emirates or Avianca LifeMiles to book a one-way international business class ticket worth $3,000-$5,000+ (getting you a crazy 3.75 - 6.25+ cpp).

These examples show how the way you use your points can dramatically change their perceived value.

Ultimately, while statement credits help lower that annual fee and earning points builds your balance, it's the smart redemption of those points, especially through those high-value transfer partners, that really unlocks the potential for profit. Consistently getting redemption values above that basic 1-1.25 cpp is key to maximizing the return on investment from a premium travel card, especially the ones with higher annual fees.

This takes a bit of learning about the partner programs and being flexible with your travel plans, but the rewards can definitely be worth the effort for those chasing maximum value. The difference between redeeming points at 1 cpp versus 2 cpp or more completely changes whether your card is just paying for itself or actually putting extra value back in your pocket.

You can calculate your CPP for any redemption that you are considering with my CPP Calculator.

Crunching the Numbers: Figuring Out Your Personal ROI

So far, we've talked about all the ways premium travel cards can give you value. But the big question is: will a specific card give you enough value to justify that annual fee? The answer is super personal and totally depends on your individual spending habits, how you like to travel, and how willing you are to actually use the card's benefits. A simple way to think about it is to calculate your potential personal Return on Investment (ROI).

Step 1: Estimate How Much Credit Value You'll Actually Use

Go through the statement credits offered by the card you're thinking about (like we did earlier). Be honest with yourself about which credits line up with things you already buy or would realistically buy.

For cards with simple, broad credits (like Venture X's $300 travel credit or CSP's $50 hotel credit), will you actually spend that amount through their portal?

For cards with lots of specific credits (like Amex Platinum), look at each one individually. If you have zero plans to join Equinox, shop at Saks, or subscribe to those specific streaming services, give those credits a value of $0 for your calculation. Only count the value you genuinely expect to use based on your normal spending.

Add up the realistic value you expect to get from all the credits you'll use. This is your direct reduction of the annual fee.

Step 2: Estimate Your Annual Rewards Earnings

Think about how much you spend each year in the card's key bonus categories (remember those 5x, 3x, 2x points?). Common categories are travel (portal vs. direct), dining, groceries, gas, streaming, etc. Also, estimate your spending in the "everything else" categories (which earn the base rate, like 1x or 2x). Calculate the total points you expect to earn each year based on your spending and the card's multipliers.

Step 3: Estimate the Value of the Perks You'll Actually Use

Try to put a dollar value on those less tangible perks:

Lounge Access: How many times a year do you think you'll actually use a lounge? What's the value of that to you per visit (maybe $30-$50 to cover food, drinks, and a quieter space)? Factor in free guest access if it applies to you (like with the Venture X).

Global Entry/TSA PreCheck/CLEAR Credits: Spread the value out over the years ( $100 GE credit / 5 years = $20/year; $189 CLEAR credit = $189/year).

Hotel/Rental Car Status: This is trickier. Think about potential savings from free breakfast (Hilton Gold via Amex Plat), room upgrades (put a conservative value on this if you get them often), or waived fees.

Travel Insurance: It’s hard to put an exact number on this one unless you actually file a claim, but acknowledge it as a valuable safety net. Maybe give it a small nominal value or just consider it a bonus.

Add up the estimated annual dollar value of all the perks you'll realistically use.

Step 4: Calculate Your Net Value/Profit

Put it all together and calculate your ROI.

If your Net Annual Value is positive, the card is likely a good financial move for you based on your projected usage.

If it's negative, the fee probably outweighs the benefits for your situation.

If it's close to zero, the card is basically breaking even, and your decision might come down to those less quantifiable things like convenience or access.

This whole exercise shows that the potential value you see on a card's marketing materials isn't automatically what you'll get. You gotta be real with yourself about your spending, travel habits, and how much effort you'll put into using the benefits.

That impressive $1500+ potential credit value on the Amex Platinum shrinks fast if you're not using those specific services or stores. Also, getting significant positive ROI, especially with the pricier cards, means you need to be proactive.

That means booking through specific portals, signing up for perks, keeping track of monthly credits, and spending some time figuring out the best ways to use your points.

Pro Tip: Ask For A Retention Offer (Year Two and Beyond)

So, you've had your premium travel card for a year or more, you've enjoyed the perks, racked up the points, and maybe even strategically used those statement credits. Then, bam! That annual fee hits your statement again. Before you automatically pay it or even consider canceling, you should see if you can get a retention offer.

Once that annual fee posts, consider giving the credit card issuer a call (or use the online chat function if available). The goal here is to politely inquire if there are any retention offers available to you for keeping your card open for another year.

Here's how this little dance typically goes:

Be Prepared: Before you dial, have a good understanding of the benefits you've actually used in the past year. Be ready for the agent to highlight the value you've received (lounge access, free hotel nights thanks to points, travel insurance savings, etc.).

Be Polite and Direct: When you get a representative on the phone, be friendly and straightforward. You could say something like, "Hi, I noticed my annual fee recently posted, and while I've enjoyed the benefits of the card, I'm just calling to see if there are any retention offers available before I make a decision about keeping the card open for another year."

Listen Carefully to the Offer: The representative might offer you bonus points, a partial statement credit on the annual fee, or a spending requirement in exchange for points. Pay close attention to the details and any spending requirements attached to the offer.

Be Prepared to Say No (and Potentially Cancel): If the issuer isn't willing to offer anything that makes the annual fee worthwhile for you for another year, be prepared to politely decline and potentially close the account. Remember to redeem any remaining points beforehand! You can also tell them that you will think about it, and call back the next day. Particularly with Amex, the offers change daily, so one day you may have a poor offer, but a much better one the next day.

Why does this work? Credit card companies want to keep good customers. Losing a cardholder means losing future transaction fees and potential interest revenue (though hopefully you're paying your balance in full!). Offering a retention bonus is often cheaper for them than acquiring a new customer.

Remember that retention offers are not guaranteed: Not every call will result in a retention offer. It depends on your spending habits, your history with the card, and the issuer's current promotions. Some banks are great about offering retention offers (Amex) while others (Capital One and Chase) are not.

Calling for a retention offer is a smart way to potentially offset that annual fee in subsequent years and continue enjoying the premium travel perks without the full cost. It's definitely worth a few minutes of your time when that fee statement arrives!

Final Thoughts: Turning That Annual Fee into a Smart Investment

The annual fees on premium travel credit cards might seem scary at first, but they can actually be a gateway to better travel experiences and faster rewards. As we've seen with the Chase Sapphire Preferred, Capital One Venture X, and Amex Platinum, these fees can lead to you getting more value back than you paid in, if you're smart about it.

The value comes from a few key areas:

Direct Credits: Getting cash back on specific spending (travel, dining, shopping, services) that directly lowers the card's real cost.

Fast Rewards: Earning tons of points or miles on travel and everyday spending, which you can then use for free trips.

Awesome Travel Perks: Getting into airport lounges, speeding through security, getting VIP treatment at hotels and car rentals, and having solid travel insurance for peace of mind.

Smart Point Usage: Knowing how to transfer points to airline and hotel partners to get way more value than just using them for cash back or basic travel bookings.

The "best" premium travel card isn't one-size-fits-all. The right choice for you totally depends on your own financial situation; how you spend, how often and how you like to travel, which airlines and hotels you prefer, and, importantly, how much effort you're willing to put into managing the card's benefits and using your rewards wisely.

That personal ROI calculation we talked about is your roadmap to figuring out if a card's benefits really line up with your life enough to outweigh the cost.

For the person who strategically uses the available credits, maxes out those bonus spending categories, takes advantage of the travel perks, and redeems points like a pro, that annual fee isn't just an expense you grudgingly pay. Instead, it becomes a smart investment.

So, the question isn't just "Should I pay an annual fee for a credit card?" but the more strategic one: "Which annual fee card offers the best potential return for me based on my personal financial and travel habits?"

By thinking about premium cards this way, you can confidently choose and use these powerful tools to reach your travel goals more easily and affordably.

Next Steps:

Check out my Cents Per Point Calculator to make sure that you are getting enough value for your points

Read my full review on the Capital One Venture X card

Read my full review on the Chase Sapphire Preferred card

Interested in applying for any of these credit cards? You can find my referral links HERE